Listen to our podcast!

Artificial intelligence trading bots promise effortless profits. Headlines hype self‑learning algorithms that can supposedly beat the market. Tools like ChatGPT can now generate trading code in seconds.

But in real financial markets, the gap between AI hype and AI reality can be expensive.

This article cuts through the noise to explain what AI for trading actually means today, how it is used across the trading lifecycle, where it genuinely adds value, and where it can fail without proper understanding. Whether you are a curious beginner or an experienced trader exploring automation, this guide will help you separate signal from noise.

What Does AI in Trading Really Mean?

At its core, AI in trading involves applying intelligent systems to tasks that once required human cognition: analysing data, recognising patterns, making predictions, managing risk, and executing trades.

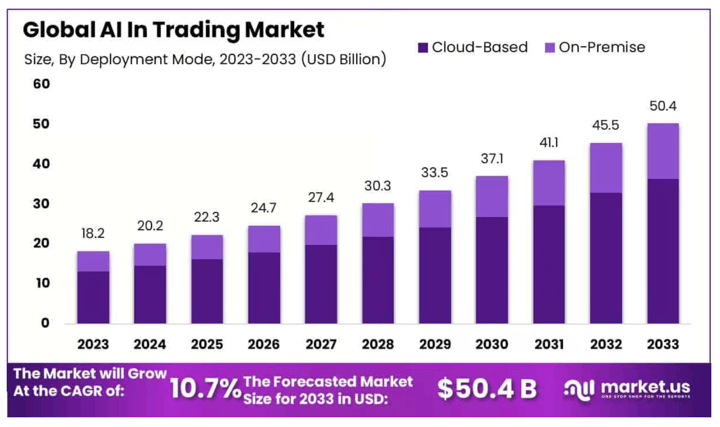

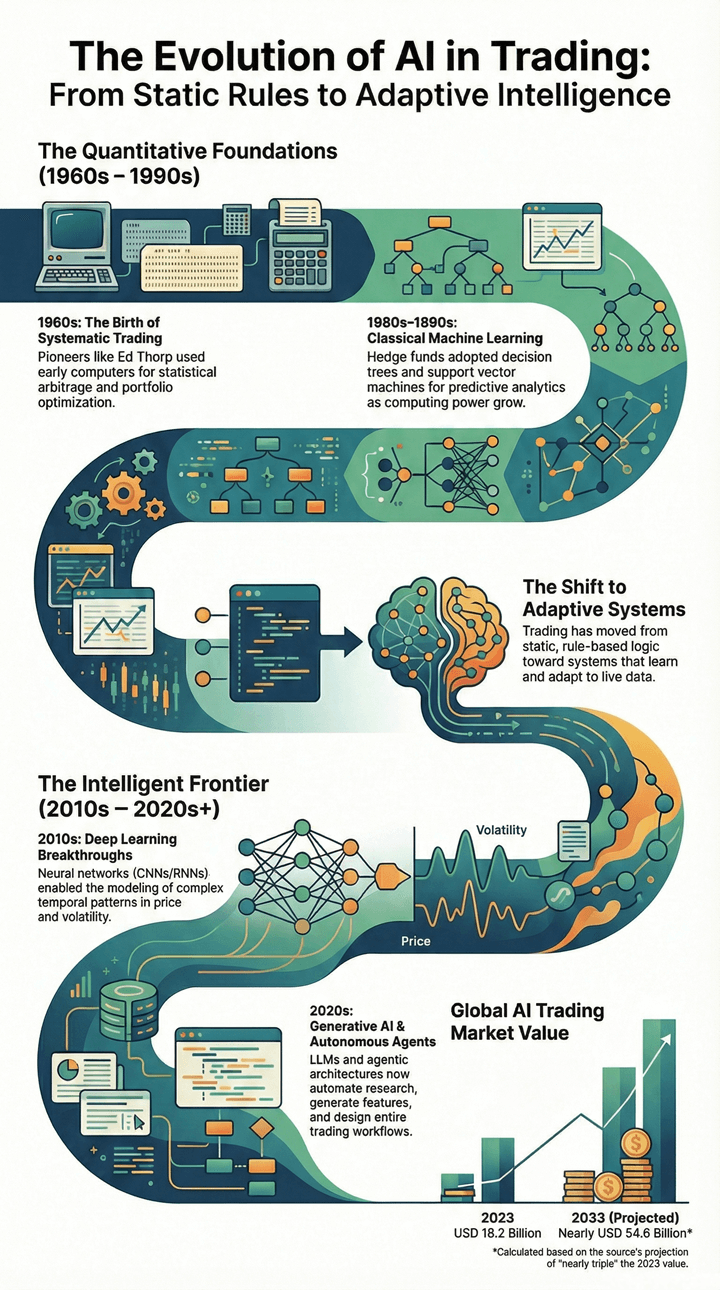

AI is a rapidly expanding segment of the fintech industry. The global AI trading market was valued at USD 18.2 billion in 2023 and is projected to nearly triple by 2033. This growth is driven by two parallel trends:

At the sophisticated end, architectures such as transformers, deep neural networks, and reinforcement learning systems analyse complex financial time series to support tasks like dynamic portfolio allocation and execution optimisation.

At the accessible end, AI assistants and no‑code or low‑code tools help traders explore ideas, analyse data, and prototype strategies more quickly than ever before.

Industry examples:

- Renaissance Technologies: Advanced statistical & ML-driven portfolio construction

- Two Sigma: Deep learning on alternative data + NLP on earnings calls

- JPMorgan LOXM : To execute client orders with maximum speed at the best price (launched in 2017)

- BlackRock : Using AI to uncover investment insights from textual data (2025 news)

- The Voleon Group : ML for microstructure prediction and execution (2019 news)

A Brief Evolution of AI in Trading

This evolution reflects a shift from static rules toward adaptive, data‑driven decision systems.

Learn more about Agentic AI Systems in Trading.

How is AI used in different steps of trading?

AI can be integrated across the entire trading lifecycle: from raw data to live execution.

1. Market Data Processing and Feature Creation

Every quantitative strategy begins with data. This includes:

- Numerical data: prices, volumes, order books, fundamentals

- Relational data: relationships across assets or markets

- Alternative data: news, earnings calls, social media, images, audio

- Synthetic data: simulated scenarios to fill real‑world gaps

Machine learning models help extract meaningful features such as momentum, volatility, regime indicators, and sentiment signals. These features form the inputs for predictive and optimisation models.

2. Model Prediction

At this stage, models forecast future behaviour such as price direction, volatility, or relative performance.

Common AI approaches include:

- Temporal models: LSTMs, transformers, CNNs

- Cross‑asset models: self‑attention mechanisms, graph neural networks

- Hybrid systems: combining time‑series and relational information

Some models focus on intermediate signals, while others directly optimize end goals such as risk‑adjusted returns. A structured progression through machine learning and deep learning models is essential before applying these systems to live markets.

3. Portfolio Optimisation and Risk Management

Predictions alone do not create profits. They must be translated into portfolio decisions.

While classical approaches such as mean‑variance optimisation and Black–Litterman remain relevant, reinforcement learning is increasingly used for dynamic capital allocation. RL agents learn policies that balance return and risk over time, adapting to changing market conditions.

If you’re looking to use AI to decide how much to invest in Gold vs Microsoft, Quantra’s AI Portfolio Management with LSTM Networks & Hyper-parameter Sweep walks you from mean-variance optimisation to LSTM-driven portfolio optimisation, with walk-forward optimisation, hyper-parameter tuning, plus live trading templates and capstone projects.

Start with a Free preview of the Course on AI Portfolio Management with LSTM Networks & Hyperparameter Sweep.

4. Order Execution

Execution is where theory meets market microstructure.

AI‑driven execution models analyse high‑frequency data to minimise transaction costs, reduce market impact, and adapt order placement in real time. Reinforcement learning is particularly well suited to this stage, where decisions must respond instantly to evolving liquidity conditions.

To go deeper into this, Quantra’s Deep Reinforcement Learning in Trading is a hands-on Python course where you apply reinforcement learning to create, backtest, paper trade, and live trade a strategy using two deep learning neural networks and replay memory. You’ll also learn to quantitatively analyze returns and risks, and finish with an implementable capstone project in financial markets.

Explore the course on Deep Reinforcement Learning in Trading with a free preview.

How AI Is Enabling Retail Participation

AI is also changing who can participate in algorithmic trading.

AI as a Coding and Research Assistant

Large Language Models such as ChatGPT and Claude are widely used to:

- Generate strategy prototypes in Python

- Explain unfamiliar code or libraries

- Explore trading ideas interactively

In practice, traders are already combining LLMs with broker APIs to build and deploy end‑to‑end trading systems, connecting research environments directly to live markets. This article is written by Pranav Lal, who completed his Certification of Excellence (EPAT) in March 2022. Pranav Lal is a seasoned information-security professional with more than two decades of experience designing and managing cyber-defence programmes for global organisations such as Lloyds Technology Center, Ernst & Young, Vodafone and the Mahindra Group.

Sentiment and Text Analysis

LLMs and NLP models are increasingly used to analyse news, earnings transcripts, and social media sentiment, providing alternative signals that complement price‑based features.

Trading Platforms and Infrastructure

Modern trading platforms support Python integration, real‑time data, backtesting engines, and automated execution. Some offer no‑code interfaces, while others allow deep customisation for advanced users.

Can You Actually Make Money With AI Trading Bots?

AI offers powerful tools but it does not eliminate risk.

Common pitfalls include:

- Overfitting: Models that perform well in backtests but fail in live markets

- LLM hallucinations: Confident but incorrect code or logic

- Hidden risk exposure: Martingale‑like behaviour that masks drawdowns

- Data quality issues: Free or noisy data leading to misleading results

- Simplified assumptions: Ignoring transaction costs, liquidity, or regime shifts

Without a grounding in machine learning concepts such as validation, robustness testing, and risk modelling, AI‑generated strategies can fail catastrophically.

AI tools amplify skill; they do not replace it.

Skills Required to Use AI Responsibly in Trading

Successful use of AI in trading typically requires:

- Clear trading hypotheses and economic intuition

- Working knowledge of Python and data analysis

- Understanding of machine learning fundamentals

- Ability to critically evaluate model outputs

- Patience to iterate, test, and refine strategies

While LLMs lower the barrier to entry, deeper control and reliability come from understanding what the models are doing and why.

Skills Required to Use AI Responsibly in Trading

Successful use of AI in trading typically requires:

- Clear trading hypotheses and economic intuition

- Working knowledge of Python and data analysis

- Understanding of machine learning fundamentals

- Ability to critically evaluate model outputs

- Patience to iterate, test, and refine strategies

While LLMs lower the barrier to entry, deeper control and reliability come from understanding what the models are doing and why.

Learning Pathways for AI‑Driven Trading

Different traders enter the AI journey at different points. Common pathways include:

- Foundations in machine learning for financial markets

- Deep learning and reinforcement learning for strategy development

- Agent‑based and autonomous AI systems for research and execution

- Short, hands‑on bootcamps focused on practical implementation

For professionals seeking a structured, end‑to‑end pathway, from quantitative foundations to real‑world deployment, comprehensive programs such as EPAT (Executive Programme in Algorithmic Trading) provide formal, career‑oriented training that integrates AI methods with market microstructure, risk management, and live trading practice.

For those who want to test the waters, you can try our AI Algo Trader Bootcamp. This is the fastest way to experience the end-to-end workflow of algorithmic trading in a structured, hands-on format.

Over four intensive sessions, you’ll learn how to go from a trading idea to a working strategy, validated with backtests, improved with the right checks, and prepared for real-world execution.

What you’ll walk away with

- A practical framework for building and evaluating trading strategies (not just theory)

- Hands-on experience with the core tools and workflows used in modern quant research

- A clearer understanding of where AI and machine learning add real leverage, and where they can mislead

- A starting point you can build on, whether that’s deeper specialisation or a full program like EPAT.

Learn more and register for AI Algo Trader Bootcamp

Final Thoughts

AI is neither a magic money machine nor an empty buzzword.

Used thoughtfully, it enables deeper analysis, faster research, and more adaptive trading systems. Used blindly, it can magnify risk and false confidence.

The real edge lies not in the tool itself, but in the trader’s ability to combine domain knowledge, statistical reasoning, and disciplined experimentation with modern AI techniques.

That combination, not automation alone, is what turns artificial intelligence into real trading intelligence.

Serious about learning?

EPAT is recommended for serious learners for those who are ready to commit to this field. A specialisation in algorithmic trading, it is often pursued by financial market participants who wish to embrace technology and AI in their work. It is a fully online course with 120+ hours of live lectures, a faculty pool of 20+ practitioners and experts from all over the world, with focus on Python and practical implementation. With dedicated mentorship, the programme enables participants of various backgrounds to join this exciting field.

Curriculum covered in EPAT is comprehensive and cutting edge, with lifetime access to improvements and additions to the curriculum.

How does QuantInsti help?

- Practical Innovation: The curriculum continuously evolves, integrating emerging financial technologies, machine learning, and crypto applications.

- Transparent & Credible Learning: A structured and practical approach that ensures real-world relevance and employer trust.

- Continuous Learning Mindset: A focus on upskilling and adaptability to stay ahead in dynamic financial markets.

- Career-Focused Approach: Every aspect of EPAT is built to enhance job readiness and professional growth.

Connect with an EPAT career counsellor to create a personalised quant career path for you